The Family Cottage

One of the great joys of summer for many Canadian families is a family cottage, cabin, or camp. No matter what name you may give the place where your clan gets together to enjoy the outdoors and each other, it’s often an important part of who you are, and how your family connects.

A lot of these properties were purchased at a time when land, even waterfront land, was inexpensive. Back when the founding family members were young, the options were endless, and capital gains taxes did not exist*.

Now, many years later, the founding family members are grandparents, or even great grandparents. The children are grown, with children – and even grandchildren – of their own. Your summer getaway may be tighter now, or organized under a strict schedule, or perhaps you’ve added an acre here, and another building there.

If your family has a hideaway like this, it’s likely that determining how best to deal with this legacy is weighing on your mind. Perhaps you’ve talked to your professional advisors, or even searched the internet for ideas on how to move ahead.

Every article, and every professional, may have a bias towards one particular direction or another. Perhaps this one tells you that the second generation of owners can’t ever get along, and it’s just best to sell it now before the fist fights begin. Maybe that one advises that you create a trust, or a corporation, to hold the asset in a structured way. Yet another might say to leave just one child or grandchild “in charge,” or even that it’s not your problem – you’ll be dead when the trouble really sets in.

There are thousands of opinions and structures that are based on the experiences of the people who have been there, done that. But the truth is that they’ve never “been there, done that” with your family. The fact pattern may line up but the reality is that your family has a unique culture, with communications, aspirations, and rules (mostly unwritten) all its own.

Here’s what I recommend:

Start with a conversation… The current owners – usually the grandparent generation – should review their own plans and concerns, determining the answers to these questions:

- How does the ongoing management of this property affect our current lives? What parts of it – financial, physical, emotional – would we want to see change before the ends of our lives? Hint: This may involve a financial & estate plan.

- What hopes or dreams do we have about this property? When we envision it towards the end of our own lives and in the continuing lives of the generations that follow us, what do we wish to see?

- If we want to see the property passed down to the generations, what concerns do we have about management?

And then, have another one… Whatever the current owners decide to do with the property is of course legally their own concern. From a family perspective however, it’s likely everyone’s concern. To maintain family harmony, the next best step should involve a conversation with the generations who have grown up in, contributed to, and loved the family cottage. I recommend that you have this conversation with each individual, and then later, together as a family.

Questions to consider asking each child:

- What does the family cottage/cabin/camp mean to you?

- What would you like to see happen, or what are your hopes around the property?

- What are your concerns about the property, both currently, and in the future?

- Do you intend to make regular use of the cottage?

- How would you split your time at the cabin with your siblings/other family members?

- How much would you be willing to commit to routine upkeep costs?

- How would you want to make decisions about what to repair and when?

- How would major decisions be made, such as whether and when to sell the cottage, when to make capital improvements, and much more?

- How would you want to solve disagreements?

From this conversation, you’ll hopefully uncover whether or not they are really connected to the property, and whether they are committed to maintaining it if they were to become owners. You’ll also find out if they are concerned about the commitment of one or more of your other children, and if they feel they have proprietary interests, over and above other children.

This could be a great time to discuss the realities of the property, from the maintenance and costs involved in just keeping it going, to the agreements between family members if there was shared ownership. Of course, there’s always that capital gains tax concern, when the property changes hands legally. It’s best to come equipped with this kind of data so everyone understands the level of responsibility required – and your professional advisors should be able to help you get quite a bit of that together.

These conversations can be emotionally trying experiences, depending on the depth of feeling involved, and how your family interacts. You may want assistance in this conversation, whether with a family therapist, a facilitator, or another professional with expertise in these kinds of family discussions.

From there create a plan… It may be the best thing for your family if the property is sold and the proceeds divided between your children. It may be best if the property is kept in the family for generations to come. It may be best that only one, or perhaps two, of your family members retain ownership and responsibility. The “right” answer is the one that works for your family.

After the hard work is completed, your professional advisors can help you determine the tax plan that will get you the result you need to move forward.

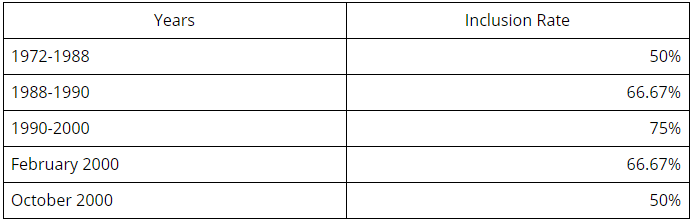

*Prior to 1972, Canada did not have a capital gains tax. In that year, the tax was introduced as a way of equalizing the tax system, removing inheritance tax, and funding our social security system. A capital gain is the difference between the purchase price and the sale price of an asset, and only a portion of that gain is considered taxable. Throughout its history the inclusion rate – the taxable amount of the gain – has changed: